CAPE Fear

What Stock Valuations Don't Price In

“America is the greatest place to do business. We have rule of law. We respect property rights.” — Warren Buffett, CNBC interview with Becky Quick, February 25, 2019

That was seven years ago. It feels like sixty.

Look at these two charts together.

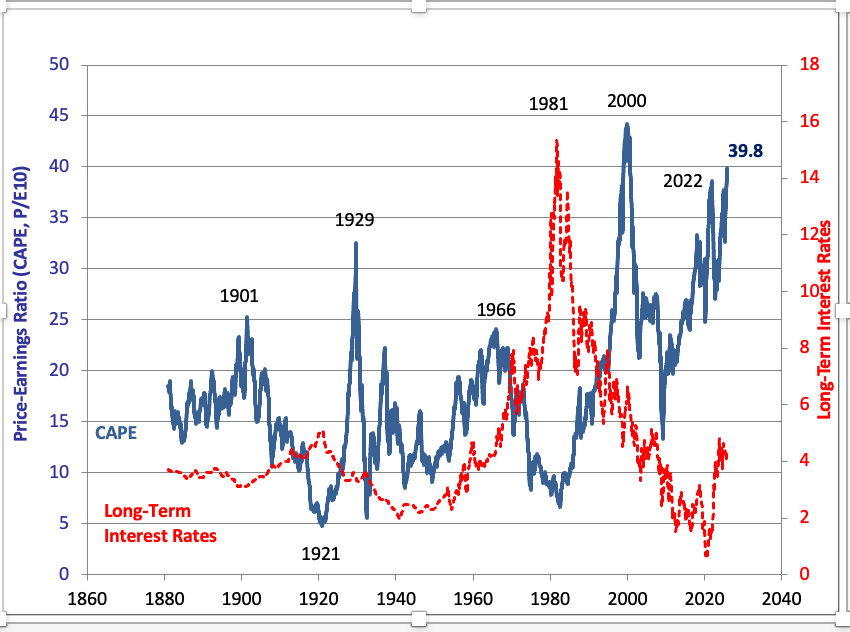

The first shows the CAPE (Cyclically Adjusted Price-to-Earnings)1 ratio at approximately 40—a level exceeded only at the peak of the 2000 stock market bubble. At these valuations, you’re not just buying future earnings. You’re buying faith in institutional permanence.

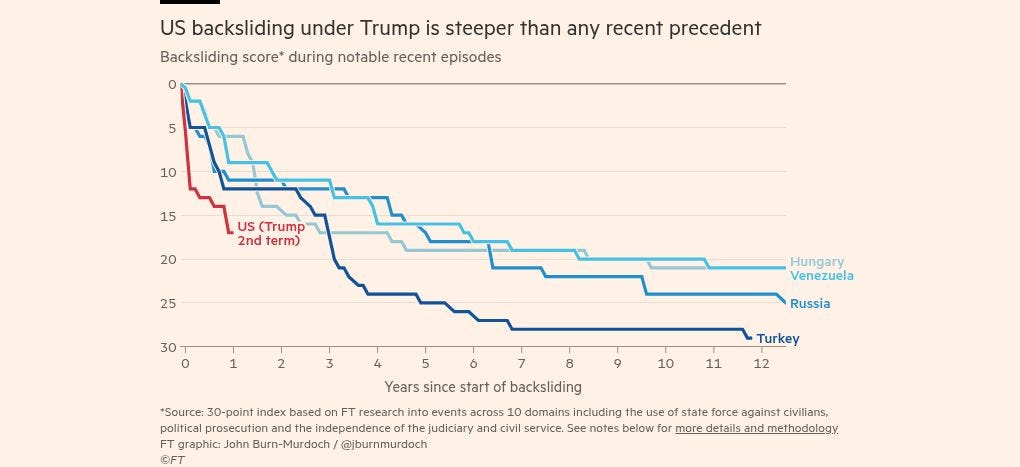

The second, from the Financial Times, tracks democratic backsliding. The US is declining - faster than Hungary, Venezuela, Russia, or Turkey did during their slides into autocracy. V-Dem and other democracy indices have already classified the US as moving toward (or already in) “electoral autocracy.”

The defunct idea at the heart of American stock market valuations is that none of this matters—that American rule of law is a permanent feature of the landscape, like Mount Rushmore. (Speaking of which, Trump loyalists have floated adding his face to it. I wish I were joking.)

It isn’t permanent. Nothing is.

As the old Wall Street saying goes, “The market can remain irrational longer than you can remain solvent.” Markets can ignore reality for a remarkably long time. But reality doesn’t return the favor.

What triggers the repricing? Not gradual erosion—markets tolerate that, like a frog not noticing it’s being boiled if the temperature rises slowly enough. They need a crystallizing event, something that forces investors to confront what they’ve been studiously ignoring. The possibilities are, unfortunately, numerous:

Federal Reserve independence dies, and it becomes apparent that interest rates are being set by the White House. When the Fed becomes a political organ, ask Argentina how that prices.

A Supreme Court ruling is openly defied. It’s already happened with lower courts—multiple times across the deportation cases, with one judge finding probable cause for criminal contempt. When SCOTUS gets the same treatment, the question shifts from “what’s this stock worth?” to “do I actually own it?”

A major CEO is indicted on pre-textual charges after criticizing administration policy. Jamie Dimon, Tim Cook, Michael Bloomberg—pick your target. CEO now stands for “Can’t Express Opposition.” We’re already halfway there.

US Government—or Trump family (it’s getting hard to tell where the Trump family’s financial interests end and the US Government begins) equity stakes are forced on major tech companies. Amazon, Alphabet, Palantir—it’s already started with Intel. Senator Rand Paul called it “a step towards socialism” (CNBC, September 3, 2025). Would you pay 40 times earnings for a company that might be forced to give the government—or the Trump family—board seats and/or equity?

US Government data becomes unreliable. The Treasury has over $1 trillion in inflation-indexed bonds outstanding, priced off the government’s own inflation calculations. When the statistics from the US Government start having the credibility of North Korean State TV, what exactly are those bonds worth?

Foreign investments in the US get confiscated. You can already hear the reasoning: “Canada has been cheating us for years—they owe us!” Paranoid? The administration seized Venezuelan oil tankers, captured the country’s president, and is now selling Venezuela’s oil directly - while blocking American creditors from recovering the billions they’re owed. Canada is considerably richer.

At some point, something on this list happens—or something nobody anticipated—and investors start heading for the exits. At a CAPE approaching 40, you need everything to go right for a decade. Every institution holding. Every norm maintained. Every check and balance functioning.

The charts say that’s not where we’re headed.

American Exceptionalism was never about amber waves of grain. It was about independent courts, honest data, and the rule of law. Strip those away and the US is just another large economy with a big military and unpredictable leadership.

You know. Like Russia.

Maybe despite America’s drift toward authoritarianism, the economy muddles through. Maybe AI really does double American economic growth, which would cover a multitude of sins. On the other hand, if the American stock market reprices to reflect the Rule of Law’s collapse - it could go down very far. My quick estimate of the current CAPE ratio for the Russian stock market: about 5.

About Steven Strauss: In the summer of 2026, he will be teaching at the Harvard Summer School, where he also taught during the summer of 2025. From 2014 to 2025, Strauss was the John L. Weinberg/Goldman Sachs Visiting Professor at Princeton University. Immediately prior to Princeton, he was on the faculty of the Harvard Kennedy School and was a 2012 Harvard University Advanced Leadership Fellow. Before Harvard, he served in the Bloomberg administration in New York City and as a management consultant with McKinsey’s London office. He holds a Ph.D. in Management from Yale University

A Note on CAPE

The CAPE ratio—Cyclically Adjusted Price-to-Earnings ratio, sometimes called the Shiller P/E after Nobel Prize-winning economist Robert Shiller—is a way of measuring whether the stock market is cheap or expensive relative to history.

The basic idea is simple: Take the current price of the S&P 500 and divide it by the average earnings of those companies over the past ten years (adjusted for inflation). Using ten years of earnings smooths out the business cycle—you’re not fooled into thinking stocks are cheap just because you’re measuring at the peak of a boom, or expensive because you caught a recession.

Historically, the CAPE ratio for the US has averaged around 16-17 (the median since 1881 is 16.04, according to data maintained by Shiller at Yale and tracked by GuruFocus). When it gets much higher, future returns tend to be lower. When it gets to 40, as it is now, you’re in nosebleed territory—paying today for a lot of optimism about tomorrow.

The ratio doesn’t tell you when a correction will happen. Markets can stay expensive for years. But it does tell you that the margin for error is very thin. At these valuations, you need a lot to go right.